Cash or accrual accounting—which method should you choose? At ProBooks NY, we discuss the pros and cons of each method with young startups every day. Here’s what we tell entrepreneurs so they can make an informed decision—including how their choice impacts business taxes. The difference between cash and accrual accounting is important to understand, whether you plan to handle your own financial statements or hire an outside professional. Each method will produce a different bottom line number. The Internal Revenue Service (IRS) requires some businesses to use the accrual method; for example, those that carry inventory over certain levels. If your business is able to choose the method it uses, it is important to understand how taxable income is determined under each method.The difference depends on the timing of when sales and purchases are recorded in your accounts. Read on to understand the implications of using each accounting method.

Cash or accrual accounting—which method should you choose? At ProBooks NY, we discuss the pros and cons of each method with young startups every day. Here’s what we tell entrepreneurs so they can make an informed decision—including how their choice impacts business taxes. The difference between cash and accrual accounting is important to understand, whether you plan to handle your own financial statements or hire an outside professional. Each method will produce a different bottom line number. The Internal Revenue Service (IRS) requires some businesses to use the accrual method; for example, those that carry inventory over certain levels. If your business is able to choose the method it uses, it is important to understand how taxable income is determined under each method.The difference depends on the timing of when sales and purchases are recorded in your accounts. Read on to understand the implications of using each accounting method.

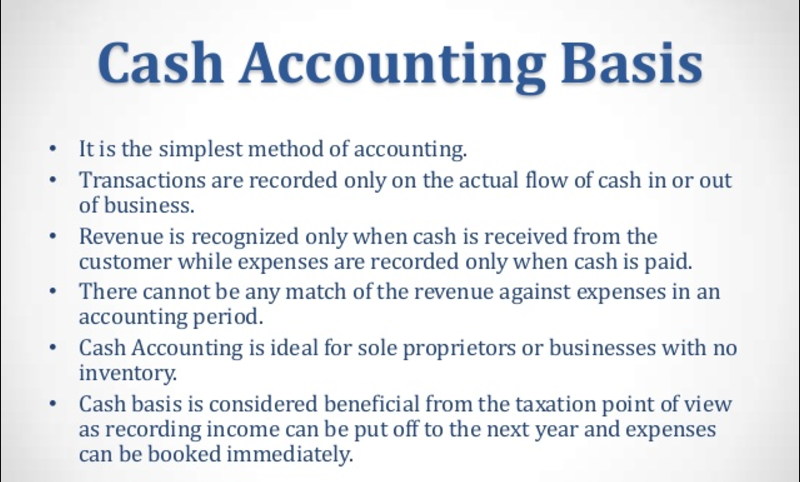

Cash-Basis Accounting

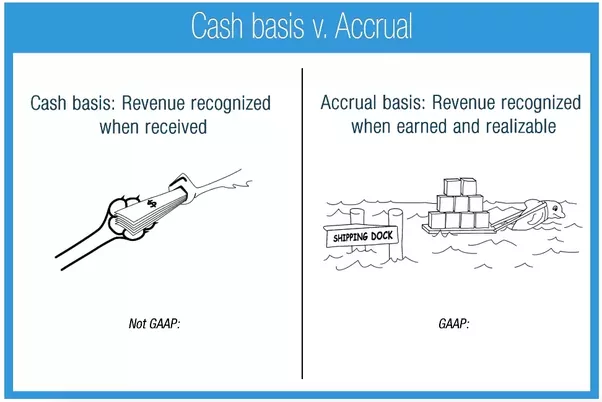

The cash accounting method reflects transactions at the time payment is actually received or made—when cash changes hands. If a monthly subscription magazine invoices its customers once a year for $60 in January, it’ll recognize the income in full when they receive the lump sum ($60 in January), instead of accounting for it each month when they ship the issue out to readers ($5 per month).

The Pros of Cash Accounting

With cash accounting, you can see the exact amount of cash you have available at any time. You can account for advanced payments when they’re received, instead of over time. Here are some additional benefits:

- Easy to see cash flow and available cash

- Cheap and simple to manage

- Easy to account for value upfront instead of over time

The Cons of Cash Accounting

Cash accounting makes it difficult to defer revenue over time. Budgeting for fluctuations is challenging when a company (like the magazine from our earlier example) receives a lot of income in a single month but delivers or performs its service on a monthly basis.

Here are some additional downfalls:

- Limits insights into long-term profitability, which can stifle growth

- Doesn’t account for value when revenue is earned?

- Difficult to create financial reports for investors and lenders

- Not enough insight to anticipate and plan for issues

Accrual-Basis Accounting

The accrual method enables businesses to record revenue and expenses when earned in real-time, even if payments haven’t hit or left an account. Accrual accounting provides a better understanding of what a business is actually worth. You may have also heard of GAAP Accounting, which stands for Generally Accepted Accounting Principles. These are the official rules for all accountants, investors, auditors, bankers and other financial professionals in the United States. Unlike cash and accrual accounting, GAAP is not an accounting method. It’s the set of widely accepted standards that ensure all companies account for their financials in the same way. Accrual is the acceptable form of accounting under GAAP’s rules. Cash method isn’t.

As an example, if the magazine, we referenced earlier used the accrual method, they could still accept lump-sum annual payments, but could also defer those funds across the entire year, when they are actually earned ($5/each month). Similarly, any purchases it made would be recognized as spending once the product or service was received or used. If it paid $120 for an annual stock photography subscription, for example, it’d account for it as a $10 expense each month.

The Pros of Accrual Accounting (and GAAP)

The extra attention you give accounting when using the accrual method (or GAAP) has plenty of upsides that help you better understand and run your business. More accurate picture of monthly income and spending to help plan ongoing and future activities:

- More control over your reported income

- Ability to anticipate cash flow trends

- Accurate budgeting with revenue recognition as the services are performed or received

- Closed-loop reporting for tracking expenses and assets back to actual earning potential

- Unbiased picture of your company’s financials–you can see what investors and other outsiders will

- Access to insights that help identify areas for improvement and hidden opportunities

- Transparency into problem areas, so you can see why you’re not hitting numbers

The Cons of Accrual Accounting (and GAAP)

Simply: it’s more difficult, takes more time, and costs more money than cash accounting. If you don’t have the experience, knowledge or proper tools to manage the accrual method or adhere to GAAP’s standards, you can make costly mistakes that the IRS might perceive as fraud.

3 Ways to Identify the Method that Makes Sense for You

Smaller businesses that satisfy the IRS’s restrictions have the choice between cash and accrual methods of accounting and aren’t required to adopt GAAP until they hit a certain level of revenue or inventory. Determining the right accounting method for your business typically comes down to three factors that affect your business’s financial complexity:

1. Income and Assets Threshold

The IRS uses a Test of Gross Receipts (better known as “the Sales Test”) to ensure companies are under the revenue threshold in order to file taxes using the cash method: Individuals, sole proprietors and small business owners (of S Corporations) must have less than $5 million in average annual sales over the last three years. Small business entities (S Corporations and C Corporations) must have less than $10 million in average annual sales over the last three years. Read more about the Gross Receipts Test on the IRS’s website here.

2. Business Milestones

Along with revenue growth, business milestones can put increased pressure on your financials. These include:

- Series A funding rounds

- Third-party auditing

- Investor board meetings/presentations

- IPO (all publicly traded companies are required by law to report their financials using GAAP)

These milestones require accrual/GAAP accounting to ensure you are providing objective information that investors and outsiders can trust. This also gives outsiders a way to easily compare across their other investment opportunities and calculate their potential risk.

3. Goals for Running Your Business

Do you want to use your accounting to run your business on a financially savvy model? Many business owners eventually realize that managing their money well is a great way to make more of it. While cash will be easier for most business owners to manage without outside help, it won’t provide the accurate data and insights into company performance that accrual accounting will. Accrual accounting will project revenue and spending more accurately, which allows for transparent budgeting. And with transparent budgeting, you can make more educated decisions faster. You’ll be a better negotiator when it comes to spending your money.

Cash and Accrual Aren’t Created Equal

But neither are businesses. In the long run, most businesses should or will be required to be on accrual, specifically for tax filing purposes. But smaller businesses with options shouldn’t use the price as the only decision-making factor. There are pros and cons to each method, so you should ask yourself a few simple questions:

- Are the extra costs worth it?

- Is there a potential that the insights and avoided mistakes will pay for themselves eventually?

- Are you okay with the cons of cash?

Conclusion

If you own a business and have chosen cash accounting, be aware that this method is only as simple as it seems until your business grows and your financial responsibilities get more complex. Contact us for a free consultation.

![]()