The most significant tax reform in more than 31 years is coming and could significantly affect your business and your bottom line. How will the plans laid out by the Trump administration and the House Ways and Means Committee come together, and how will potential policy changes affect you and your business?

Two things about you:

- You’re busy.

- You want to save on your business taxes.

The great thing about taxes (no, really!) is that taking steps to save money come tax time will ensure your business’ financial health all year long. By the same token, the beginning of the next tax year is the best time to see whether you’re maximizing your deductions and ask an expert about additional ways to save.

Good news!

Even though you’ve already earned most of your income for the year, you still have time to lower the taxes you owe. And as a business owner, you have even more options for lowering your taxable income than individual taxpayers do. That’s because the IRS and U.S. Tax laws allow business owners to deduct most of the expenses they incur from doing business.

Is it Worth it?

Having a good handle on your taxes means two things: 1. You’ll avoid penalties and 2. you’ll pay less each year. That’s money you’ll be able to reinvest in your business. So taking the time to figure out your deductions and claim them is absolutely worth the opportunity cost associated with managing your taxes.

Remember that the tax code is complicated, so we highly recommend working with a CPA who specializes in your type of business. Many entrepreneurs aren’t aware of all the power they have to actually dictate their tax responsibilities. Having a good handle on your taxes means you’ll save money, allowing you to reinvest in your business.

This article outlines:

- 7 different types of business taxes to anticipate in advance

- 3 essential things you’ll need to take advantage of tax deductions

- 8 best practices for saving on your taxes – from filing on time to maximizing deductions

A FEW THINGS TO KEEP IN MIND

As a business owner, you have a huge amount of control over your business expenses—which means you can also dictate your tax deductions. But there are other important factors affecting your tax obligations that you should be aware of.

Your Entity Type Matters

Many businesses have some choice over their entity type, but the process of switching business entities is complex. Consult an attorney. Many companies start life as an LLC. This can make a lot of sense from a tax perspective. But there may come a time when incorporating will save you money. For example, if you and a few partners have an LLC or S corporation, all of the business income passes through to the owners. This is also known as a flow-through entity. The income is only taxed once, which is a good deal for many people. But at a certain threshold, it might be a better deal to structure your business as a C corporation. While your business’s income will be taxed as an independent entity, and its investors taxed separately, the first $50,000 of your income is taxed at a rate of 15%, as opposed to 35%, for owners in the highest tax bracket.

Beware of the Alternative Minimum Tax

The alternative minimum tax can affect individuals, LLCs, partnerships, and corporations. The IRS calculates the alternative minimum tax separately from your regular tax liability and with different rules. Then you pay whichever tax bill is higher. The alternative minimum tax, or AMT, was originally designed to make sure that very wealthy people and corporations couldn’t use legal deductions to get out of paying taxes. That sounds good in theory, but the AMT is now increasingly affecting the middle class.

The alternative minimum tax can affect individuals, LLCs, partnerships, and corporations. The IRS calculates the alternative minimum tax separately from your regular tax liability and with different rules. Then you pay whichever tax bill is higher. The alternative minimum tax, or AMT, was originally designed to make sure that very wealthy people and corporations couldn’t use legal deductions to get out of paying taxes. That sounds good in theory, but the AMT is now increasingly affecting the middle class.

Trapped in a shadow tax system. The Alternative Minimum Tax operates as a parallel tax system that requires Americans to calculate their tax burden under two separate structures. Under the AMT, taxpayers with many children, a second mortgage, high state taxes, or who otherwise claim various tax benefits they thought the tax code was intended to encourage may be trapped into recalculating their taxes under a different set of rules and paying much higher taxes.

Certain expenses, such as property taxes, that are deductible under the regular rules are not deductible under the AMT. This also means that deductions might not matter if you’ll end up having to pay the AMT regardless. The takeaway: Consult a tax professional.

Tax Law isn’t Getting Less Complicated & it is Always Changing.

Major legislation, court cases, IRS rulings and even natural disasters can all affect tax law. Many changes to tax law benefit taxpayers—but only if you know about them and have time to respond. Waiting for a once-yearly meeting with your accountant may not leave you enough time to learn about and act on these opportunities. For example, in 2005, after hurricanes Katrina, Rita and Wilma struck the U.S., the government created a number of short-term tax savings opportunities. Also, charitable contribution limits were raised for individuals and corporations, but only through the end of 2005. In order to keep pace with changes to tax law, it’s important to have periodic check-ins with your tax specialist throughout the year.

Types of Business Taxes

Businesses are on the hook for a variety of taxes. Job creators have had to deal with the highest corporate tax rate in the industrialized world. It’s unlikely that all of them will apply to you, but it’s essential to identify those that do. In our experience, a surprising number of entrepreneurs are unaware of at least one type of tax they’re responsible for—and that means paying penalties, in addition to back taxes and interest.

1 Income Taxes

Every individual taxpayer already knows about federal and state income taxes. But the way that you pay them as a business depends on your entity type. If your company is a sole proprietorship, partnership, limited liability company or S corporation, you (and any partners or shareholders) will pay income taxes via your personal tax return. If your business is a C corporation, the business pays its own taxes and then each employee and investor pay their own additional layer of tax on income that has passed through payroll or as a dividend.

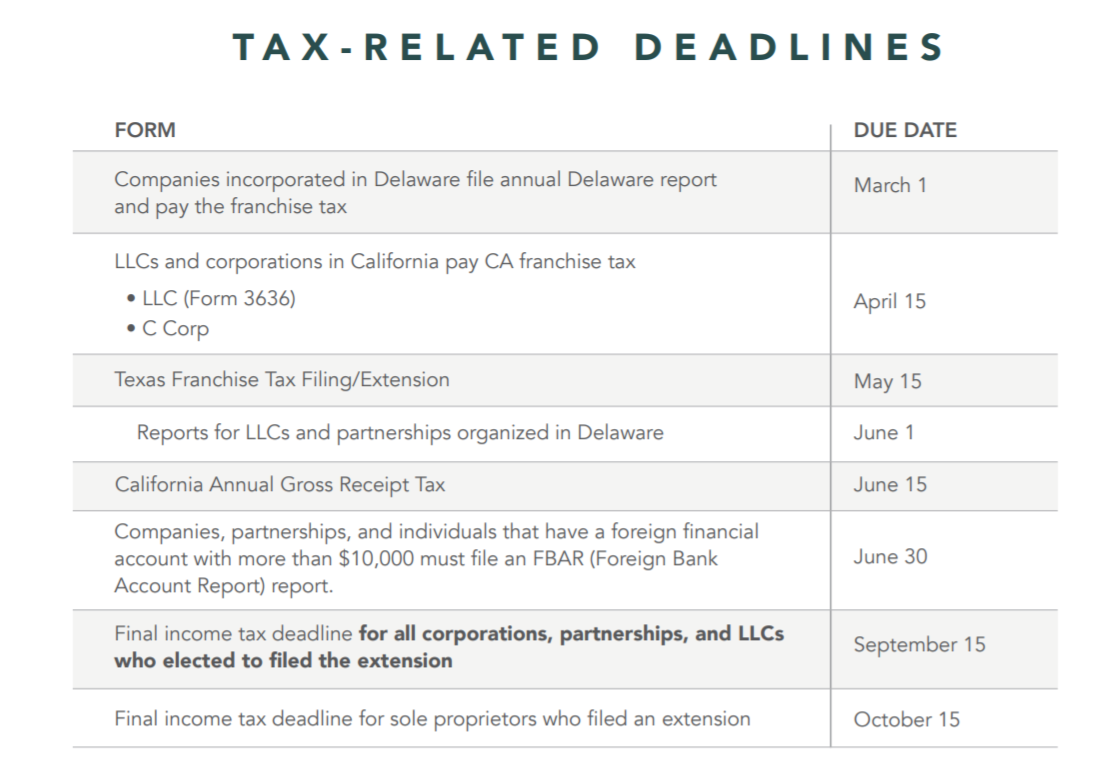

2 Franchise Tax

Most U.S. states require businesses to pay franchise taxes if they have a “nexus” there. Unlike income tax, a franchise tax is often, but not always, based on the net worth of the business. Take Delaware: The majority of companies in the U.S.are incorporated in the First State, partly because it doesn’t have corporate income tax. It does have a significant franchise tax, though. States with higher corporate income taxes usually have low or no franchise taxes, and vice versa.

3 Employment Taxes

If you have employees, you are required by the Federal Insurance Contributions Act, better known as FICA, to withhold income taxes and employees’ shares of Social Security and Medicare. As a business, you pay the employer’s share of FICA, plus state and federal unemployment taxes while your employees will pay these on an individual basis each month, via paycheck withholdings. If your business is incorporated, you count as an employee and owe these taxes—even if you’re the only employee. If you are self-employed, you owe self-employment taxes (equivalent to both the employee and employer share of FICA) on your net earnings.

4 Sales Taxes

If your company does business in a state that has sales tax and you sell goods or services, you may have to collect sales taxes from your customers on each transaction. You may face penalties for failing to collect this tax on behalf of the state. Here are 4 questions that startups and small businesses should know about state sales tax.

5 Excise Taxes

Depending on your type of business, you might be required to pay excise taxes, which affect a wide array of activities. Common examples of excise taxes are those imposed on fuels, highway use by trucks, cigarettes and alcohol and hotels. Excise taxes are integrated into the listed price of the good or service. For example, the list price of a bottle of liquor includes the excise tax. Then, the convenience store pays excise taxes to the state for all the liquor it sells.

6 Gross Receipts Tax

A handful of states tax the total gross revenues of a company, regardless of the source of revenue. A gross receipts tax is similar to a sales tax, but it is levied on the business rather than the consumer.

7 Net Worth Tax/Capital Tax

Unlike income tax, a net worth tax is a levy on the total value of personal assets, including owner occupied housing; cash, bank deposits, money funds, and savings in insurance and pension plans; investment in real estate and unincorporated businesses; and corporate stock, financial securities, and personal trusts. Liabilities, such as mortgages and loans, are deducted. There is no federal net worth tax; in states that have this tax, you typically pay either a net worth tax or income tax, whichever is higher.

WHAT YOU NEED IN ORDER TO TAKE DEDUCTIONS

If you want to take deductions (who doesn’t!), the IRS requires you to keep specific records. It’s not that the IRS does not trust you, it just needs evidence that you’ve earned the deductions you claim.

1 A bookkeeping system.

The IRS wants you to closely track your income and expenses, but every business should do this anyway. There are many accounting solutions out there, and the best ones (including our’s) give you concrete data to make smart decisions. Your tax accountant will need a balance sheet, an income statement and a cash flow statement. If you bought, sold or disposed of any capital assets during the year, your accountant will also want to see capital-asset activity for the year.

2 Receipts and other proofs of your expenses.

Your CPA will thank you for storing and categorizing these digitally rather than using the old shoebox method. It’s a bonus if your bookkeeping solution also stores your receipts.

3 Certain expenses require specific records.

A common example is using a personal car for business purposes. In this case, track your business mileage in a diary or log book and tell your employees to do the same.

WAYS TO SAVE

Finally, the good stuff!

There are hundreds of ways for small businesses to save on taxes. We’re just going into eight big ones. That’s because 1. this guide is free and 2. we’ll say it again—consult a CPA who understands the tax deductions and credits that apply to your business type and industry.

1. File on time (but ask the IRS to waive penalties if you don’t)

This is number one for a reason. Surprised? Filing on time, or for an extension, is not going to lower your taxable income. But if you fail to do so, you could face some expensive consequences:

- Late payment penalty: typically ½ of 1% of your unpaid taxes, per month

- Interest on taxes owed: the federal short-term rate plus 3% with interest compounding daily

- Late filing penalty: usually 5% of the unpaid taxes for each month or part of a month that a tax return is late. The penalty starts accruing the day after the tax filing due date and will not exceed 25% of your unpaid taxes. This is the big one—always file on time or file for an extension. These always-avoidable expenses can add up quickly. If you think you’ll need extra time, filing for an extension will allow you—and your tax preparer—the time it takes to claim the deductions available to you, rather than racing to meet a deadline. Remember: You still have to pay on time even if you file an extension.

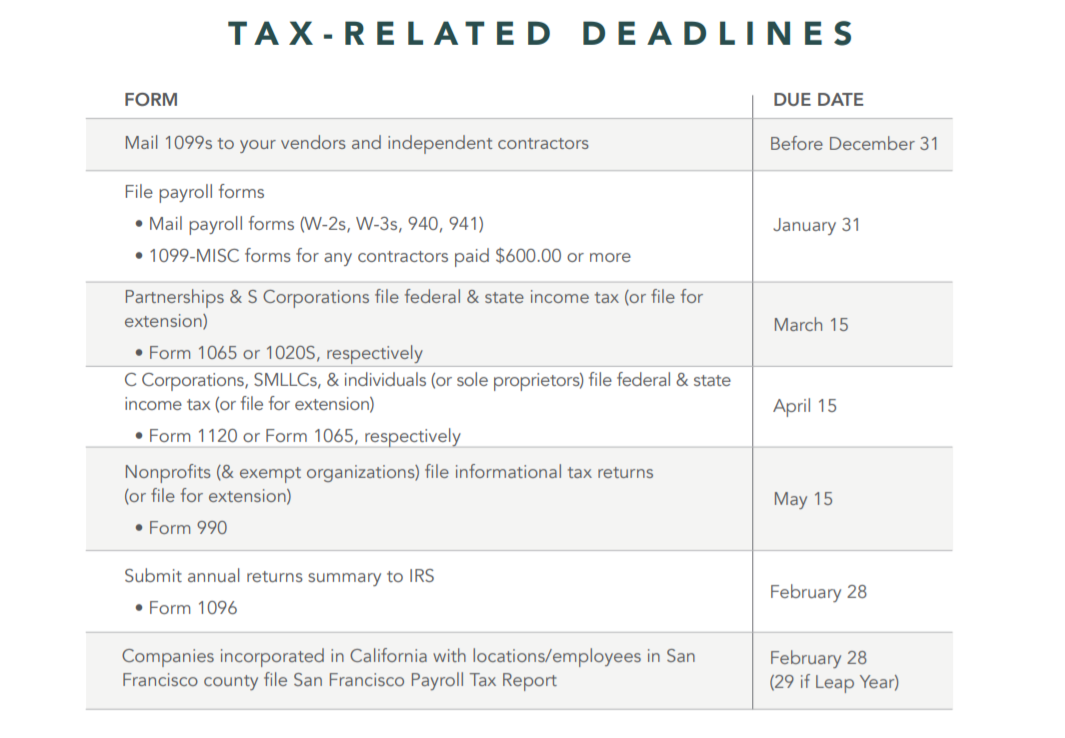

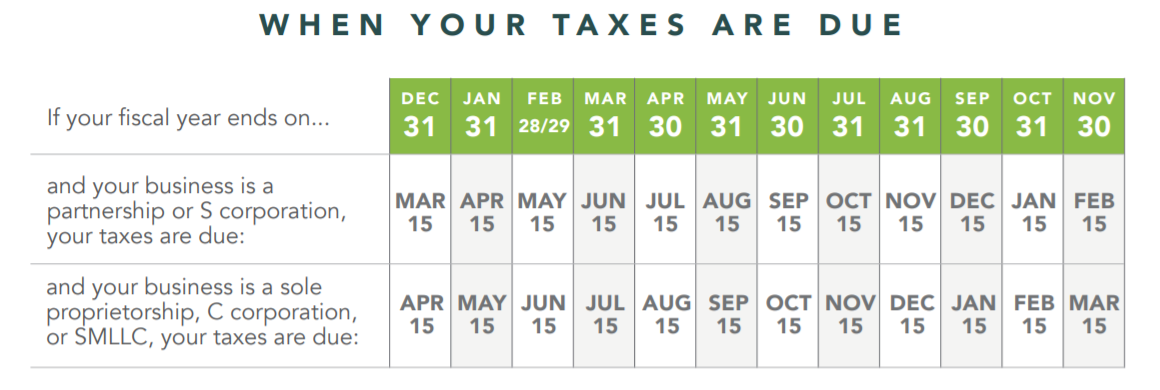

If your company is incorporated and your tax return or extension is due two-and-a-half months after year end or if your business is a partnership, sole-proprietorship, or LLC and your taxes or extension three-and-a-half months after year end, there are a few other filing deadlines you should be aware of, too

For example at Probooks NY, we specialize in bookkeeping and taxes for SaaS companies, restaurant industry, startups and professional services firms.

If your fiscal year is different than the calendar year, just use this handy chart.

If you think you’ll need an extension, file for it as soon as possible—there’s no disadvantage if you end up filing on time, but if you miss the filing deadline, you’re on the hook for a hefty penalty. Planning ahead is always a good thing, especially when it comes to taxes, so use this IRS lifeline to buy yourself the time it takes to ensure that you have everything that your CPA needs for maximum efficiency. Say you have a major life crisis and you miss your deadline and you don’t file for an extension. Or maybe you file on time, but you weren’t aware that you had to pay a certain tax. You can still ask the IRS to waive the penalty. It may work out, it may not. But it’s worth asking.

- Treat yourself to some equipment or improvements

The 179 deduction is your friend.

Typically, you deduct the costs of buying new business equipment by claiming a depreciation allowance over 5-7 years. It’s not a bad deal, but it means your deduction is spread out over time. However, section 179 allows you to accelerate the deduction so you can get the entire tax benefit in the same year you started using your new equipment. This is known as first-year expensing, and it applies to equipment that is bought, leased, or financed. Before you break out your credit card, know the federal limits to the 179 deduction. (States may have different limits or may not allow a 179 deduction at all.)

- The dollar limitation. For the tax year 2016, the IRS will allow you to deduct $25,000 under section 179. Congress often adjusts this at the last minute to favor the taxpayer: In 2014 they raised the limit to $500,000.

- The dollar limitation part 2. In 2016, if the property you want to deduct under section 179 costs more than $200,000, your $25,000 limit is reduced dollar for dollar: If you buy something that costs $205,000, your new dollar limitation is $20,000. Again, these numbers could change drastically in your favor if Congress raises the dollar limit.

- You still have to pay taxes. Your 179 deduction for any taxable year can’t be more than your business income–you can’t use the 179 deduction to spend your way out of paying taxes. But if you have expenses left over, you can carry them over to next year.

You’re only allowed to claim the 179 election for the year that the equipment is purchased, financed, or leased and put into place. So what kinds of things count?

“Tangible personal property” used in business, whether purchased, financed, or leased:

- Equipment and machines, such as computers

- Office furniture

- Personal vehicles used for business

- Vehicles used exclusively for business

- Software

Some purchases aren’t eligible for the 179 election. But you can still use the traditional system of capitalizing and depreciating your equipment over a period of time for things like:

- Land and buildings that you own, including parking areas

- HVAC equipment

- Anything located outside of the United States

- Furnishings for a company apartment

- Used equipment

- Home office? Maximize that deduction!

26 million Americans have home offices, but just 3.4 million taxpayers claim home-office deductions. That’s silly. Not everyone who has a home office will meet the criteria, but for those who do, the home office tax deduction packs a huge savings punch.

While this deduction typically doesn’t apply to C Corp employees, it’s great for many sole proprietors and LLC partners. Whether you rent or own your dwelling you can claim this deduction on a personal income tax return, if:

- You use your office to manage a trade or business (if you’re an interior designer or an IT consultant who does most of your work onsite this still counts) and

- There is no other fixed location where you conduct substantial administrative or management activities.

If your home office is just a nice-to-have, but you don’t really need it, you shouldn’t claim the deduction. To write off a home office, it must be used exclusively and on a regular basis.8 It can be your office or a studio or the exam room where you meet with clients or patients.

The key is that the area must be used only for work—not occasionally for exercising or guests. It doesn’t have to be the entire room, but the area must be used only for work, and the boundaries must be clear.

You don’t have to use your office every day, just on a regular basis. If you use your office to meet with clients, a few meetings over the course of the year won’t cut it. And if you sometimes work from home at the table in your guest room, don’t try to claim it. However, if your home office is a separate structure, if you use it to store inventory, or if you operate a daycare, the rules are a bit more flexible.

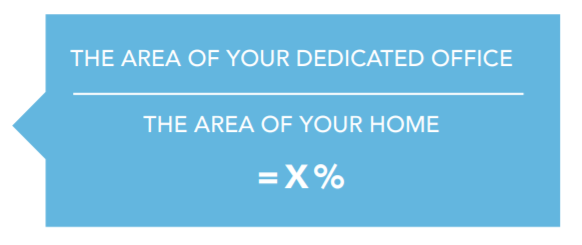

The home office deduction is actually several separate deductions! This deduction is based on a simple calculation:

This percentage is applied to a bunch of little deductions that add up quickly. So if the area of your office is 10% of your home, you’ll be able to deduct 10% of many of your regular expenses including:

- rent or home mortgage interest

- utility bills

- home repairs

- depreciation…so break out your tape measure—you’ll need to know the area of your home and the percentage that comprises your office.

Since 2013, the IRS has simplified the rules so that individuals have had the option to simply deduct $5 per square foot for up to 300 square feet, or $1500. But if your office is larger or if all your deductions would amount to more than $1500 you can still go the traditional route.

- Consider adding to employee benefits instead of bonuses

Payroll taxes are expensive, and they only go up with each new employee added to the roster—and then again at raise time. Because payroll taxes are proportional to an employee’s income, you’ll pay more taxes each time a person gets a raise or a bonus.

A tax-saving alternative to yearly bonuses is to contribute more to health insurance costs or other benefits.

Look at it this way: you could get everyone a $500 bonus come December. But then each employee would have to pay income tax, FICA tax, and Medicare tax on those wages. And you would have to pay the employer share of FICA, Medicare and possibly federal and state unemployment taxes as well. But if you contributed $500 to insurance premiums, an HRA, or even bus or parking passes, everyone will be spared income tax, FICA, Medicare and unemployment taxes.

At a certain point, your employees are going to want raises. But strategically adding to benefits can be a way to earn employee goodwill and rein in your tax obligations.

The IRS is strict. There are rules about this. You can’t buy people cars or houses, which are taxable the same as income. Consider:

- Contributing to employee health insurance premiums

- Setting up employer-owned health reimbursement accounts to cover employees’ qualified medical expenses

- Contributing to employee-owned health savings accounts

- Providing public transportation passes (up to $130 per month, after which you’ll pay taxes)

- Constructing an on-site gym (memberships to separate gyms don’t count, unfortunately)

- Contribute a percentage to your employees’ 401(k)

- And speaking of retirement plans….

- Maximize your retirement plan contributions

There may be no better investment than tax-deferred retirement accounts. They can grow substantially because they compound over time free of taxes. Everyone can take advantage of this way to save, and there are several ways to go about doing it. Most people can contribute to more than one! The 401(k) If your business is profitable, you can set aside income in a qualified retirement plan. As an employer, 401(k) contributions can help you out in several ways:

- You can claim deductions for the matching contributions you make to each employee’s 401(k), including your own.

- You’ll lower your personal taxable income by contributing to your own 401(k) with every paycheck.

- When you (and your employees) pay into a 401(k), you’ll be deferring the taxes on those earnings. You will not be taxed until you start withdrawing from the account, which is usually at retirement.

And don’t forget: Creating—and contributing to—an employee 401(k) is also a great way to build loyalty among your staff. Do your best to contribute the maximum amount allowed to your own 401(k) so you reap the benefits. In 2016, you can contribute $18,000. If you are 50 or older, you can contribute $24,000.

The IRA

Individual retirement accounts, or IRAs, come in a few different flavors.

You have until April 15 to make contributions to any kind of IRA for the previous tax year.

This is great news because it allows you to lower your taxable income even after the tax year is over. But the sooner you get your money into the account, the sooner it has the potential to start growing.

You can contribute a maximum of $5,500 to an IRA for 2016, plus an extra $1,000 if you are 50 or older.

Traditional IRA

You contribute money to a traditional IRA before taxes like you would with a 401k through your employer and similarly, the money you withdraw at retirement gets taxed as income. In 2016 and 2017, you can contribute $5,500 a year or $6,500 a year to a traditional IRA. If you also have a Roth IRA, your total contributions to both plans can’t exceed those limits!

Roth IRA

In 2016, a married couple that makes less than $193,000 a year, or a single person who makes less than $131,000 a year, can contribute to a Roth IRA. This is unlike most retirement accounts because you contribute funds to it after taxes—the advantage to this is that you won’t pay taxes on the principle when you begin to withdraw from this account. This will lower your tax obligations after retirement, like a gift to your 70-year-old self. Remember, if you also have a traditional IRA, your total contributions to both plans can’t exceed the annual limits!

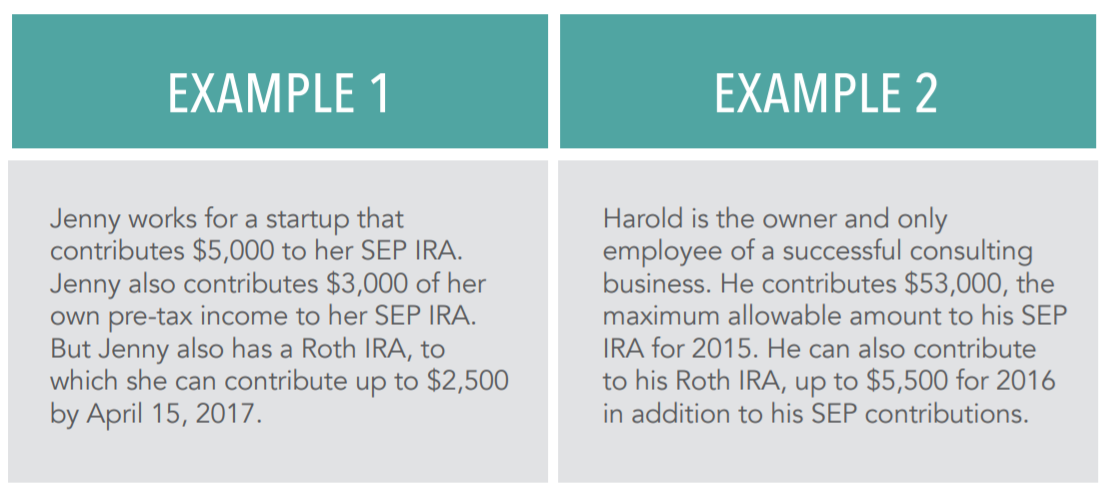

SEP IRA

If you have a sole-proprietorship, partnership, or LLC, definitely consider a SEP IRA. A SEP IRA is a type of traditional IRA. Any business owner with one or more employees, or anyone with freelance income, can open a SEP IRA. Contributions, which are tax-deductible for the business or individual, go into a traditional IRA held in the employee’s name. If you’re self-employed, use a special calculation to determine contributions for yourself.

The money in a SEP IRA is not taxable until withdrawal. Employer contributions made under a SEP plan do not affect the amount you can contribute to an IRA on your own behalf. You can contribute much higher amounts to a SEP IRA than you can to a traditional or Roth IRA:

- 25% of compensation

- $53,000 (for 2016 and 2017 and subject to annual cost-of-living adjustments for later years)

- Take steps to defer or lower your business income

It makes sense to defer your income if (1) you use cash accounting and (2) you think you will be in the same or a lower tax bracket next year.

If your main goal is to lower this year’s taxes, defer your income. If you use cash accounting, you have a couple of options for delaying this year’s income until next year. This will lower the amount of taxes you have to pay, but only for the time being.

- Send out your final invoices in the last few days of your fiscal year.

You won’t receive payment from your customers or clients until next year, so you won’t be on the hook for that income. Don’t abuse this tactic. Flexing your invoice date at the end of the year is okay, but don’t hold onto invoices for months to avoid paying taxes. Again, this only works for businesses that use cash accounting. Accrual businesses don’t have this option.

- Pay next year’s bills early.

Most businesses and individuals have predictable bills each month. Can you pre-pay January’s bills in December? If you can afford it—and you use cash accounting— you’ll be able to deduct a few of next year’s expenses for this tax year. Keep in mind that you won’t be able to benefit from those deductions the following tax season, so think ahead.

- Take the long view.

It doesn’t make sense to defer your income this year if you are only going to be hit with a higher bill the following year. And if you think that may happen, you may want to do the opposite: Ask your customers if they’d like to prepay you, before next year. If this presents a tax benefit to them, or if you offer a discount, this could help lower next year’s tax obligations.

We don’t recommend paying your bills late because that’s no way to run a business. If your business uses accrual accounting, you can’t take advantage of these options. But one way any business can lower their taxable income and boost employee morale is end-of-year bonuses!

In section 5, we suggested adding to employee benefits rather than bonuses as a way to save on payroll taxes. That’s a good strategic move. But giving every employee a few hundred dollars at holiday time (distinct from performance-based bonuses) can be a low-maintenance way of lowering your taxable income in one fell swoop and spreading some holiday cheer.

Speaking of employee morale and holiday cheer….

- Donate to charity

The money, supplies, and property your company donates all can count toward your deductible expenses. And you control the timing! Donating to charity is a great way to involve your employees and positively affect your workplace culture. There are so many ways to go about doing this. You’ll get the tax deduction no matter what, so get your team’s input on how they would like to donate and volunteer.

- Make a company donation to coincide with an employee volunteer day at a food bank, soup kitchen, shelter, hospital or school.

- Match employee donations to charities of their choice.

- Sponsor a 5K in your community that benefits a non-profit or hospital and then volunteer on the day of the event. (This is also a great PR opportunity—remember your company t-shirts!)

- Collect employee donations of canned food, toys, or professional clothes for relevant charities in-office. Then, include a monetary, tax-deductible donation along with the goods.

Cash donations are great, but to get the most from a charitable deduction, donate stock or property that has appreciated, or increased in value. That way, you can claim a tax deduction for your gift’s value on the date you gave it and avoid paying capital gains tax on the increased value. Never donate stock that has gone down in value!

REMEMBER

- You must have a receipt to back up any contribution, regardless of the amount.

- You can’t donate away your entire income. Generally, your charitable contributions can’t exceed more than 50% of your adjusted gross income. This limit drops to 30% if you’re donating the property.

- Donate to IRS-approved nonprofits, such as charities, schools, and religious organizations. Political contributions don’t count.

Capital gains are the profits from the sale of a non-inventory asset that you purchased for less than you sold it. The most common capital gains are realized from the sale of stocks, bonds, precious metals, and property.

- Sell losing investments to offset gains

This strategy only affects personal income taxes, not business taxes. But if your personal income is high enough, selling losing investments is a good way to offset your taxable gains. That’s because income you lose offsets income you gain dollar for dollar.This strategy is referred to as loss-harvesting.

If you invest in stocks, you’ll have the occasional loser. That’s no fun, but you can use the losses to lower your taxes. That does mean selling your stock at a loss. Once you realize a capital loss, you can use it to offset any capital gains you have.

This also allows you to avoid paying tax on those capital gains.

If you have more capital losses than gains, the IRS allows you to use up to $3,000 of that excess loss to offset your taxable income. If you have more than $3,000 in excess losses, it can be carried over to the next year. You can carry over losses year after year for as long as you live.

Capital losses can wipe out a significant amount of your tax liability, but be careful: If you buy back the same or a “substantially similar” investment 30 days before or after taking it as a tax loss, the IRS won’t let you claim the losses.

As with every other strategy in this guide, be sure to consult a tax expert!

CONCLUSION

Taxes, especially for businesses, are only getting more complicated each year. It’s important to be aware of ways to save and avoid paying more than you have to but having a tax professional who understands your business type and industry is essential. Ultimately, the key to a stress-free tax season is excellent year-round accounting. When all of your expenses, bills, and assets are kept up to date, you won’t be faced with unpleasant surprises come tax time. The tax code is long because it has been written in large part by special interests, especially corporations, shaping it to suit their needs. And the Republicans may succeed at tax reform overhaul where they failed at health reform.

Taxes, especially for businesses, are only getting more complicated each year. It’s important to be aware of ways to save and avoid paying more than you have to but having a tax professional who understands your business type and industry is essential. Ultimately, the key to a stress-free tax season is excellent year-round accounting. When all of your expenses, bills, and assets are kept up to date, you won’t be faced with unpleasant surprises come tax time. The tax code is long because it has been written in large part by special interests, especially corporations, shaping it to suit their needs. And the Republicans may succeed at tax reform overhaul where they failed at health reform.

Our friendly financial consultants can help you understand which type of accounting and tax filing solution is the best fit for your business. SCHEDULE A CALL TODAY